cemagraphics

Wednesday’s wild session in stocks added to September’s collection of big market swings, and CFRA’s Chief Investment Strategist Sam Stovall sees five factors holding sway over the market.

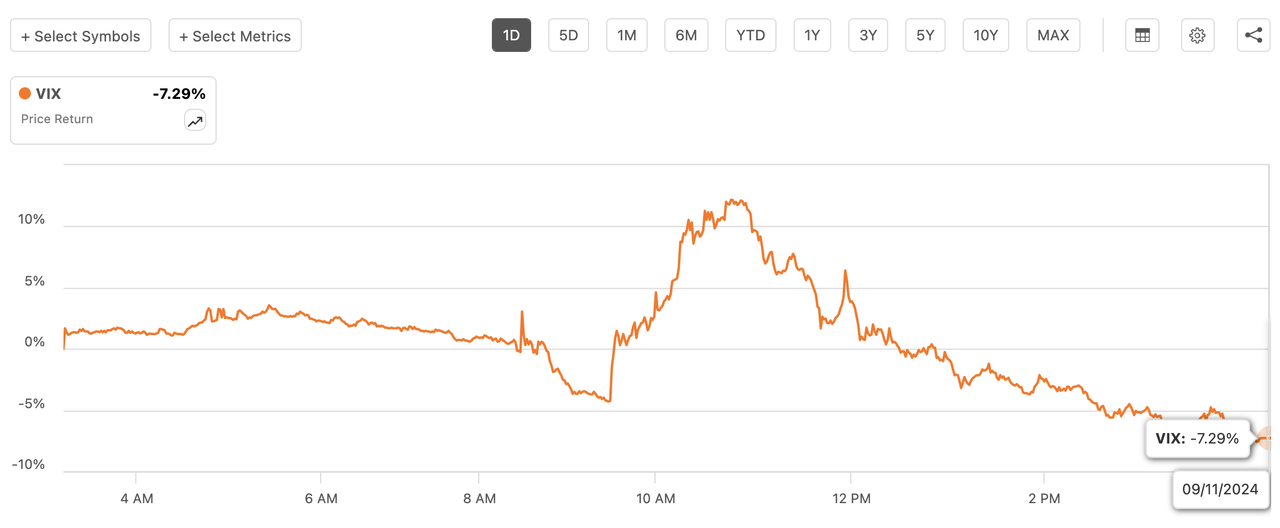

The S&P 500 (SP500), Nasdaq Composite (COMP:IND) and Dow (DJI) closed higher Wednesday after each slumped more than 1%. The moves followed a larger-than-expected rise in the August core consumer price index. Wall Street’s volatility gauge (VIX) also was lashed about, surging more than 12%, followed by an 8% drop before paring the loss to 7.3% by day’s end.

“Why does the equity market volatility persist? Take your pick of possible causes,” Stovall said in a Wednesday afternoon note. He listed five potential causes:

- 1) The Consumer Price Index reading “adds credence to the forecast of only a 25-bp cut at next week’s Federal Open Markets Committee meeting, rather than the earlier hoped-for cut of 50 bps,” he said.

The August CPI report showed core inflation rose 0.3% M/M, higher than the 0.2% estimated rate. The report drove down the odds of a rate cut of 50 basis points to 15% while the chance of a smaller cut of 25 basis points increased to 85%. The FOMC meets Sept. 17-18.

- 2) The most recent jobs reports have further raised the risk of recession, the strategist said.

The August jobs report showed payrolls rising by 142K, below the 160K consensus. July’s jobs report sparked recession fears as payrolls growth missed expectations and the unemployment rate rose to 4.3%. July payrolls were eventually revised down, to 89K from 114K. The unemployment rate slipped to 4.2% in August.

- 3) The Japanese central bank’s expectation to continue hiking rates should lead to a continuation of the yen (USD:JPY) carry trade unwind, Stovall said.

The decades-long yen carry trade, under which investors borrow yen at ultra-low rates near zero to invest in assets with higher yields, such as U.S. bonds and stocks, was disrupted early last month. The Japanese yen (JPY:USD) began quickly rising against the dollar (DXY), spurred by the Bank of Japan in late July raising interest rates, upending global markets.

- 4) “The outcome of last night’s presidential debate has increased the likelihood of Democrat victory,” Stovall said, referring to the U.S. presidential election in November.

One measure indicating markets deemed Vice President Kamala Harris the winner of Tuesday night’s debate against Republican and former president Donald Trump, shares of Trump Media & Technology (DJT) sank 10% on Wednesday.

- 5) “The market continues to be buffeted by uncertainty in this traditional period of pre-election seasonal softness that will abate once the election is over,” Stovall said. “History reminds us that the S&P 500 (SP500) gained an average of nearly 3% in the final two months of election years since 1992, along with price increases for all sizes, styles, and sectors.”

Investors can monitor major equity averages through ETFs including (SPY), (QQQ), (DIA), (IVV), (QLD), (VOO), and (DDM).

from Business – My Blog https://ift.tt/4jcFs3B

via IFTTT

No comments:

Post a Comment