photoschmidt

Only a few months ago, Aeva Technologies, Inc. (NYSE:AEVA) was trading around $0.50 with limited market interest in the Lidar stock causing NYSE listing issues. Now, the 4D Lidar sensor company has suddenly announced a big trucking deal and the stock has soared back above $1. My investment thesis is still Bullish on the stock, but Aeva is still far away from moving away from a pre-revenue company.

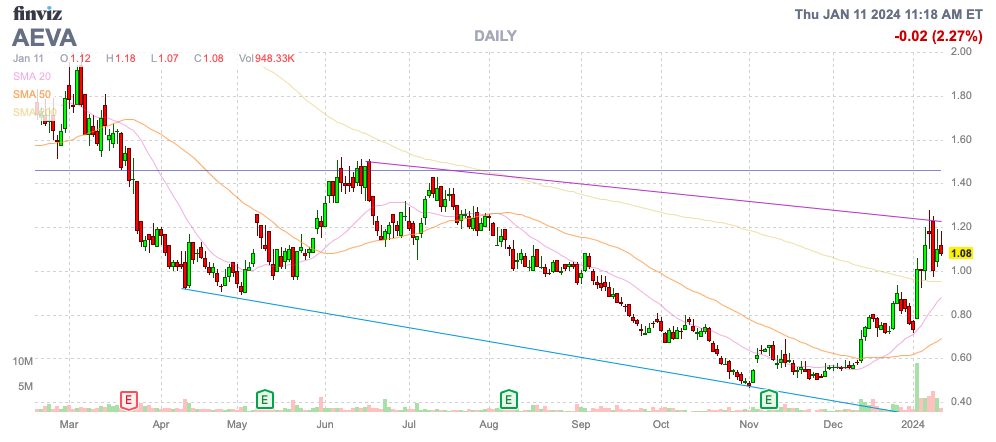

Source: Finviz

Still Far Away

During CES, Aeva announced a potentially big deal with Daimler Truck to integrate their Lidar sensors in a collaboration with Torc Robotics to enable SAE Level 4 autonomous vehicle capabilities beginning with the Class 8 Freightliner Cascadia truck platform. Though not included in the announcement, media reports suggested the deal value amounts to $1 billion in future orders over an unspecified period of usually at least 5 years.

The problem here for Aeva is the distant timeline. The partnership might begin during the current quarter, but Daimler Truck’s production won’t ramp up until 2027, and the deal requires customers to buy self-driving trucks with the Lidar sensors included.

As mentioned by Aeva in the press release, the company replaced an existing supplier of 3D Time-of-Flight, Long-Range Lidar with their FMCW technology. According to a prior press release, Luminar Technologies (LAZR) formed a partnership with Daimler Truck back in late 2020, which include Daimler acquiring a minority stake in Luminar.

While replacing an industry leader in Luminar is a positive sign, it’s also part of why the market is now hesitant to aggressively invest in the Lidar stocks. Mainly, the deal is 3 years away from volume revenue, but also signs exist an existing supplier can be replaced. Though the automotive sector is traditionally a difficult sector to replace existing suppliers unless going out years into future vehicle models.

Back in Q4, Aeva also announced official deals with May Mobility and Nikon. The company now has the production deals lacking in previously years to provide a level of future viability.

The May Mobility deal is interesting, with transit programs already providing 350,000 rides in Ann Arbor, MI; Arlington, TX; Grand Rapids, MN; and Sun City, AZ, with additional deployments planned to begin in 2024. The deal doesn’t start production ramp until 2025, leaving shareholders again with a lengthy time before volume sales hit the books.

More Dilution Ahead

The biggest problem facing Aeva is that the company is just now announcing deals several years away from meaningful production ramps. The Lidar company has had to raise substantial additional capital since going public to fund ongoing losses.

Aeva reported Q3 ’23 revenues of just $0.8 million, actually dipping from $1.4 million in the prior-year period. The company lost $30.3 million in the quarter and had negative free cash flow of $29.1 million.

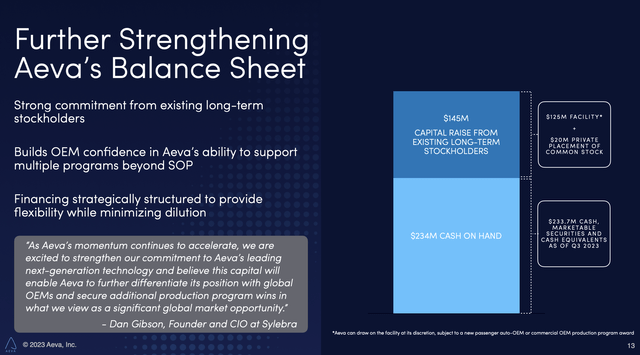

The company ended Q3 with a cash balance of $234 million before the recent capital raise. Aeva is still running at nearly $120 million annual cash burn rate with limited revenues until at least 2026, or beyond.

Back in November, the company announced agreements to raise up to $145 million in additional capital in combined private placement of $20 million and a non-voting preferred shares facility of $125 million. The capital raises come from existing long-term stockholders and strategically position Aeva to win additional OEM programs.

Source: Aeva Q3’23 presentation

Aeva had a share count of 223 million shares, placing the market cap at a minimal $250 million prior to the recent capital raise. The company ended up selling 37 million shares at only $0.58 per share to boost the fully diluted share count to 260 million shares before even accounting for the preferred shares and 15 million warrants issued with an exercise price of only $1.

The biggest question to investing here is the binding nature of the Lidar deals, considering the major automotive deals involved replacing existing ToF Lidar competitors, Investors have to wait years to ensure these claimed orders of $1 billion materialize.

Analysts only forecast 2024 revenue of $14 million, with a jump over $50 million in 2025, but the only major Tier 1 deal doesn’t ramp-up production until 2027. Aeva has a long path ahead to cover ongoing cash burn rates before any of the recent deals ramp into material-enough revenues to cut the cash burn.

Takeaway

The key investor takeaway is that Aeva Technologies, Inc. has been on a surprising roll, with recent Lidar sensor deal announcements after the stock was left for dead in mid-2023. The stock likely has more upside in 2024, but investors still have a long road ahead with questions on further dilution and whether these deals will actually materialize as presented.

from Finance – My Blog https://ift.tt/hVWiJIP

via IFTTT

No comments:

Post a Comment